Tax Audit and ITR Deadlines for FY 2024-25: Key Extensions by the IT Department The Central Board of Direct Taxes (CBDT) has announced a deadline extension for the filing of Income Tax Returns (ITR) and audit reports for FY 2024-25 (AY 2025-26). The due date for filing the Return of Income under Section 139(1) of the Income Tax Act has been extended to October 31, 2025 for assessees referred to in clause (a) of the Explanation. This affects a significant and broad-based group of taxpayers including businesses, professionals, and individual taxpayers, and otherwise represents continuing changes to the compliance framework of the Income-tax Act of 1961.

What has been extended? As per section 44AB of the Act and corresponding provisions, certain taxpayers would be mandatorily required to get their books of account audited and thereby file their audit report and ITR with respect to the said by specified date. The main changes are as follows:

For a taxpayer who is not liable for audit (i.e. salaried individuals, HUF, AOPs whose account is not liable for audit), the ITR time limit has been increased upto 15 September 2025 from 31 July, 2025. If a taxpayer's accounts are subject to audit, the date for providing audit reports (in some situations) has now been changed to 31 October 2025, up from 30 September 2025 (in which the extended date will apply). Some reports under section 92E (across international/specified domestic transactions) will also apply to the later date, but the official deadline to do so has yet to be introduced in all cases. For a simplified summary, refer to below:

Category of Taxpayer Original Deadline (FY 2024-25 / AY 2025-26) Revised Deadline* Remarks Accounts not required to be audited ITR – 31 July 2025 ITR – 15 September 2025 Extension notified by CBDT. Accounts required to be audited Audit report – 30 Sept 2025ITR – 31 Oct 2025 Audit report – 31 Oct 2025 (for many)ITR – 31 Oct 2025 Applies to audit cases; CBDT has extended, and some High Courts have intervened. Accounts requiring TP/section 92E reporting ITR – 30 Nov 2025 (typically)Audit report – one month earlier No uniform extension announced for all cases yet Particular TR/92E cases may have different timeframes.

*Revision pertains to official extension notifications or widely reported practice

Also Read: Cash Sales/Bill limit in GST and Income Tax

How this extension might be concerning Although the extension of the tax audit and ITR filing deadline for FY 2024–25 has been welcomed, experts indicated this is still partial and inconsistent.

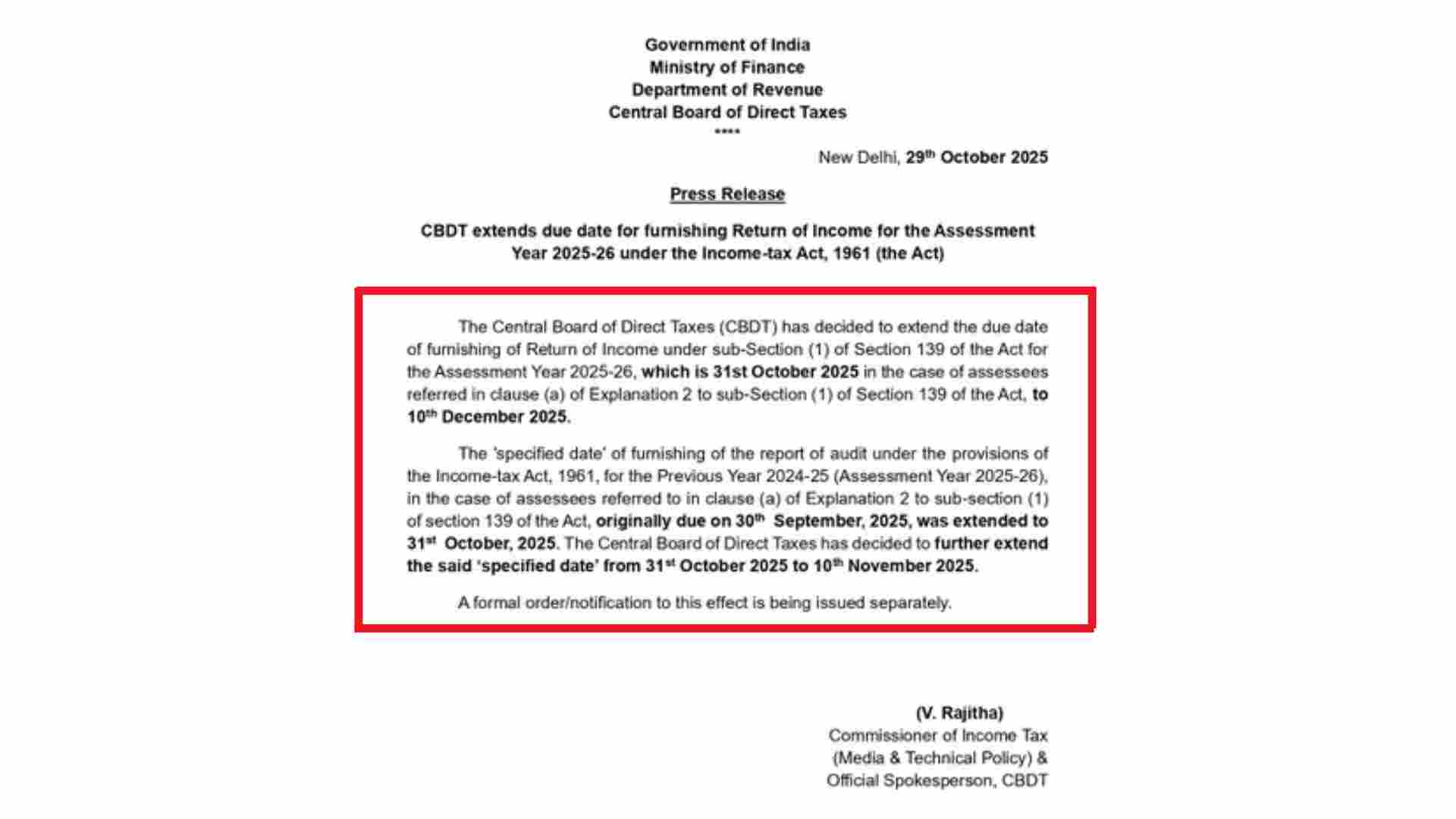

Chartered accountants expressed concerns that taxpayers under transfer pricing (TP) audit provisions in a 92E scenario were excluded from the relief. These taxpayers are still subject to the 30 November 2025 deadline while everyone else has a 10 December 2025 deadline even though taxpayers under TP scenarios have complicated compliance. CA Deepak Chopra called the extension "partial relief," stressing the unfair disparity for companies transacting internationally. CA Gaurav Makhijani pointed out that this inconsistency leads to an “absurd situation” where entities with higher compliance obligations have shorter deadlines. The mismatch between audit report and ITR filing due dates may create confusion, compliance pressure, and risk of penalties or litigation. Data shows that corporate filings of the ITR to the tax authority remain low, indicating continued challenges in meeting the deadline. The experts stated that the CBDT needs to uniformly extend the deadline for the ITR filing across all regimes so that the compliance burden is minimised, fair to the taxpayer, and the efficiency of the tax authority is retained. Why the extensions? Numerous factors have been behind the request for these extensions:

Specifically, the rollout of revised ITR forms, revised reporting formats and additional disclosure requirements created an added operational burden for both taxpayers and added stress to the e-filing system. There were also technical glitches, delayed utility software, mismatches in the AIS vs. Form 26AS data and other issues caused by various professional bodies (such as ICAI) requesting additional time. The Central Board of Direct Taxes recognized the potential for a “smooth and convenient filing experience” in these systematic pre-requisites. What it means for taxpayers Taxpayers who are salaried individuals, HUFs and other similar taxpayers who do not require an audit are now given until 15 September 2025 to file their ITR each year. Otherwise, it would become a “belated” return under section 139(4), which could attract a late-filing fee under section 234F and could impact some taxpayers from carrying forward certain losses. In cases that require an audit, Entities or professionals whose accounts are to be audited must first file the audit report (usually Form 3CA/3CD or 3CB/3CD) by the due date as per the revised norms (for most cases, 31 October 2025 ), followed by filing the ITR by the due date as per the ITR. If the audit report is not filed in time, then filing the ITR will not be possible as a regular filing, and the taxpayer will incur the consequences of filing a belated return. In terms of 92E / TP reporting, taxpayers engaged in international or specified domestic transactions to produce a TP audit Report (Form 3CEB) must vigilantly consider the sequence of required due dates, as the regular filing of ITR is due on 30 November 2025; however, some of the professional bodies are requesting to extend all due dates uniformly. Suggested Read: Understanding 115BAC of Income Tax Act: New Tax Regime Explained

Conclusion The extended deadlines set by the CBDT for filing for FY 2024-25 are a comfort to taxpayers, and in particular, to taxpayers who have audits, new forms, new disclosure requirements or all three. The extensions should be seen as a chance to develop better compliance systems, not a further delay. Proper planning, early engagement with tax professionals and immediate data handling are still important.

Adequate utilization of the revised deadlines can provide taxpayers sufficient time to facilitate compliance, oversee timely filings and limit the possibility of penalties, interest and/or relinquishing benefits. Taxpayers should align their deadlines internally with the new deadlines and begin reviewing filing obligations and their need for an audit, so they comply with the Income-tax Act, 1961 and have an easier time working with the tax administration system this year.

FAQs 1. What are the new tax audit and ITR deadlines for FY 2024-25? The Income Tax Department has extended the tax audit and ITR deadlines for FY 2024-25. For taxpayers who do not need an audit, the last date to file the ITR is 15 September 2025. Taxpayers who need an audit, both the audit report due date and the last ITR filing date, have been extended to 31 October 2025, according to the CBDT notification.

2. Why did the Income Tax Department extend tax audit and ITR deadlines for FY 2024-25? The purpose of extending the deadlines is to provide relief to taxpayers who face difficulties related to new ITR forms, updates to the portal, and data mismatches related to AIS/Form 26AS. The CBDT said that it took multiple representations made by professional bodies into account before extending the deadlines.

3. Who is required to undergo a tax audit for FY 2024-25? Tax audits under section 44AB apply to businesses and professionals - taxpayers, when the turnover or receipts exceed the specified thresholds. Taxpayers would have to submit a tax audit report on or before the due date if they want their ITR filing for FY 2024-25 to be valid.

4. What if I miss the ITR filing due date for FY 2024-25? If you have missed the due date to file the ITR for FY 2024-25, your return is "belated". Filing the return late will lead to several consequences and penalties under sections 234F, cannot carry forward certain losses, and may result in a higher degree of scrutiny by the Income Tax Department.

5. Where can I find the most recent CBDT notification regarding the tax audit declaration and the revision of the due date for ITR? You can find the latest CBDT notification on the official Income Tax Department website or through PIB.gov.in press releases.

People Also Ask 1. What is the extension date for 2025? The ITR filing due date for FY 2024–25 (AY 2025–26) is now 15 September 2025 for individuals not requiring a tax audit.

2. What is the time limit for a tax audit? The due date for the tax audit report is 31 October 2025, for FY 2024–25.

3. Is ITR filing time extended? Yes. The return filed by the ordinary taxpayers have been made last date from 31st July, 2025 to 15th September, 2025.

4. Can I file an ITR after 31 July? Yes, you can file a belated return upto 31st December, 2025, but you have to pay late fees and interest thereon.

5. How can I avoid a tax audit? To avoid tax audit one has to keep turnover less than Rs. One crore (or less than Rs. 10 crores in case the cash transactions are less than 5%) and keep proper records.

.png)

-compressed.jpg)

.jpg)