Allowances and Exemptions Under Section 10(14)(ii) of the Income Tax Act Salary structures are usually confusing since they contain a number of different elements other than the basic pay. While many employees understand the taxable and non-taxable parts of their income, most do not explore the allowances available under different sections of the Income Tax Act. One of the most beneficial but less understood sections is Section 10(14)(ii) . This provision deals with allowances granted to employees specifically for performing official duties. These allowances offer tax benefits, reduce the financial burden on employees, and improve take-home income.

This blog breaks down Section 10(14)(ii) in simple terms. You will understand the types of allowances covered, the rules to claim exemptions , the eligibility criteria, and the documentation needed to ensure these allowances are correctly reported in your tax filings. The purpose is to help every salaried employee understand how this section works and use it effectively for tax planning.

What is Section 10(14)(ii)? Section 10(14)(ii) deals with allowances which are given by employers to assist employees in the discharge of their official duties. These allowances are not meant for personal use. They are given so employees can complete their work efficiently without paying out of pocket.

The law says that the amount exempt under this section should be equal to the actual expenses incurred for the specific official purpose. If an employee receives more than what is spent, the balance becomes taxable. This ensures that the exemption remains fair and strictly related to professional duties.

For example, if an employee receives Rs 4,000 as conveyance allowance and spends Rs 2,700 for office travel, only Rs 2,700 will be exempt. The remaining Rs 1,300 becomes taxable.

Why Section 10(14)(ii) Matters for Employees Many employees do not realize that they can reduce their taxable income by understanding the allowances under this section. These allowances provide dual benefits. Employees receive financial help for official work and also get partial or full tax relief on the amount spent for that work.

This provision is especially valuable for roles involving frequent travel, office-related expenses, research duties, or uniform requirements. When used correctly, it lowers the tax liability and improves take-home salary.

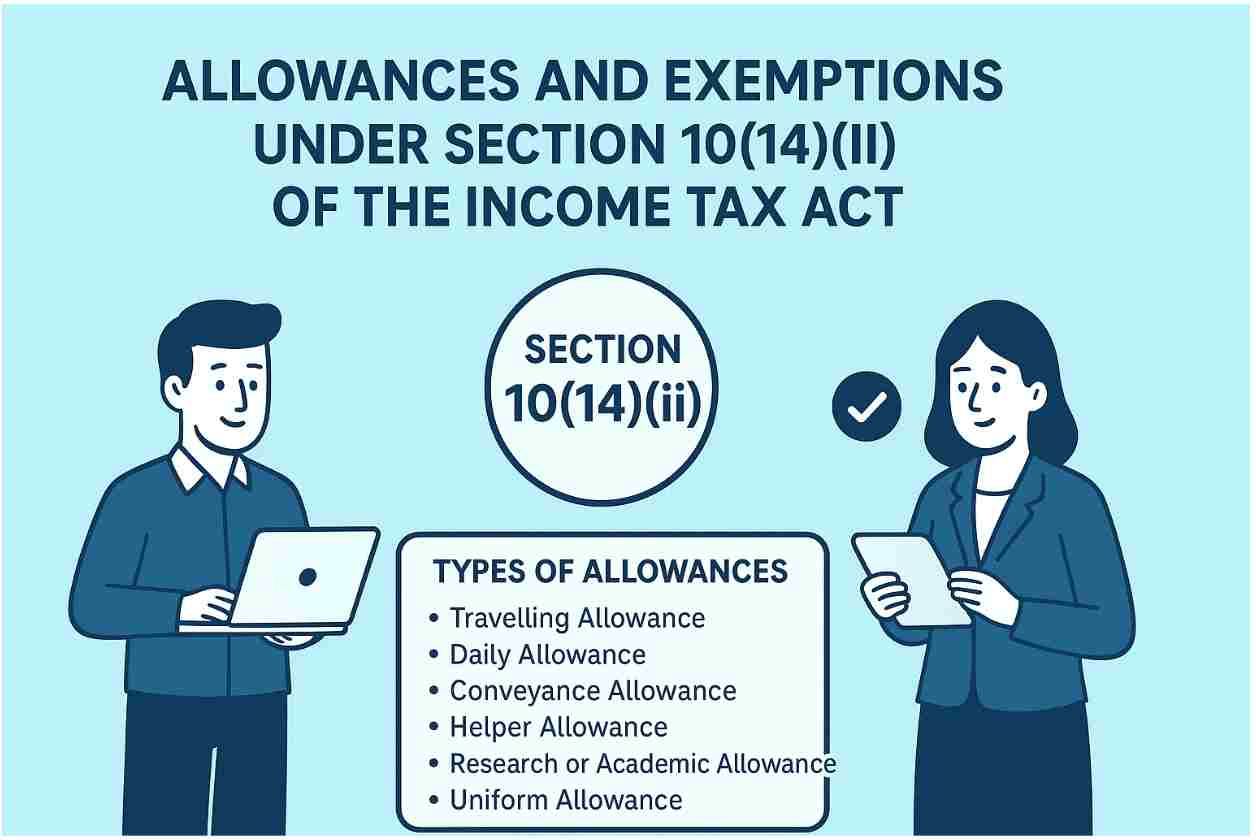

Types of Allowances Covered Under Section 10(14)(ii) Below are the common allowances that fall under this section. Each of these allowances serves a specific official purpose, and the exemption applies only to the extent of actual spending.

1. Travelling Allowance Travelling allowance is used in cases where the employee travels on official purposes, like field visits, inspections, meetings, or tours to work. The only cost that can be exempted relates to such travel.

2. Daily Allowance Daily allowance is provided to cover the cost of food, local transportation, and incidental expenses when making official tours. It assists the employees in covering their daily costs when they are not at their regular workplace.

3. Conveyance Allowance Conveyance allowance is paid when employees must travel within the city or between office locations for official duties. It is different from transport allowance, which is for commuting between home and office.

4. Helper Allowance Some roles require employees to hire a helper or assistant to perform specific office-related tasks. The allowance paid for hiring such help is exempt to the extent of the amount spent.

5. Research or Academic Allowance Research projects, training, seminars, and educational activities usually need financial funding from teachers, researchers, and academic professionals. The amount allowed as expenses on these purposes is free, where the employee actually expends it on work-related academic pursuits.

6. Uniform Allowance Uniform allowance helps employees cover the cost of purchasing and maintaining the uniform required for their job. Only the portion spent specifically on uniforms qualifies for exemption.

For the complete list of allowances covered under Rule 2BB , you may refer to the official Income Tax India portal.

Requirements to Claim Exemptions In Order to avail exemptions under Section 10(14)(ii), employees are subject to some conditions. These conditions ensure that the exemption is granted only when the allowance is used for its intended official purpose.

1. Allowance should be for Official Duties The allowance must be connected to the employee’s job responsibilities. If the allowance is meant for personal use, it does not qualify under this section.

2. Proof of Actual Expenditure Employees are required to retain good bills, receipts, or documents of support that they utilized the allowance to carry out official work.

3. Only Actual Amount Spent Is Exempt If an employee spends less than the allowance received, the unused portion becomes taxable.

4. Allowance Must Be Listed Under Rule 2BB Only the allowance mentioned in the Income Tax Rules can be claimed under this section.

Tax Exemption Rules Under Section 10(14)(ii) The exemption rules under this section are clear and easy to follow:

1. Exemption is Limited to Actual Expenses If an employee claims more than they spend, the excess becomes taxable.

2. No Standard Limit There is no fixed upper limit for exemption. It depends purely on the amount spent on official duties.

3. Documentation is important Employees need proper proof to justify the amount claimed.

4. Allowances Must Be Purpose-Specific The exemption applies only when the allowance is used for the exact purpose for which it is granted.

Table: Allowances Under Section 10(14)(ii) Allowance Purpose Exemption Limit Travelling Allowance Official tours and travel Actual amount spent Daily Allowance Daily expenses during duty travel Actual amount spent Conveyance Allowance Travel for office work Actual amount spent Helper Allowance Hiring a helper for official tasks Actual amount spent Research / Academic Allowance Research and academic work Actual amount spent Uniform Allowance Purchase and maintenance of uniform Actual amount spent

Claiming Exemptions under Section 1014(ii) In Order to claim exemptions, follow these steps:

1. Maintain Expense Records All bills, receipts, travel slips, and documents that justify expenses should be kept by the employees.

2. Submit Expense Records All documents should be submitted to the HR or payroll team before Form 16 is prepared.

3. Check Your Form 16 Employees must ensure the exemption is reflected correctly in the section “Allowances exempt under Section 10”.

4. Report the Exempt Amount in ITR Employees also need to correctly declare the exempt income in the stated section of the Income Tax Return form during the tax filing .

These exemptions must be reported properly in your ITR step-by-step filing guide. Refer to our blog on How to File Income Tax Return Online .

Frequently Asked Questions (FAQs) 1. Does Section 10(14)(ii) provide an exhaustive exemption of the allowances? No, only the amount spent on official work is exempt. The unused portion is taxable.

2. Do employees need bills to claim these exemptions? Yes, supporting documents are essential. The exemption is not possible without evidence.

3. Can self-employed professionals claim these exemptions? No, these are only permitted for the salaried staff.

4. Is HRA covered under this section? No, HRA applies to Section 10(13A), not Section 10(14)(ii).

5. Does this section contain a set exemption limit? No, there is no fixed cap. Exemption equals the actual amount spent.

Conclusion Section 10(14)(ii) assists employees to deduct their taxable income by giving them an option of exemptions on work allowances. These allowances. These allowances include traveling, daily allowances on tours, conveyance, research, and uniforms. This section is beneficial in that employees are able to ensure that they are well documented and utilize the allowance in carrying out official tasks.

The knowledge of these rules will guarantee proper tax planning and will avoid mistakes at the time of tax filing. Employees who regularly incur expenses for office work should use this provision to reduce their tax liability and improve their financial planning.

.png)

-compressed.jpg)

.jpg)