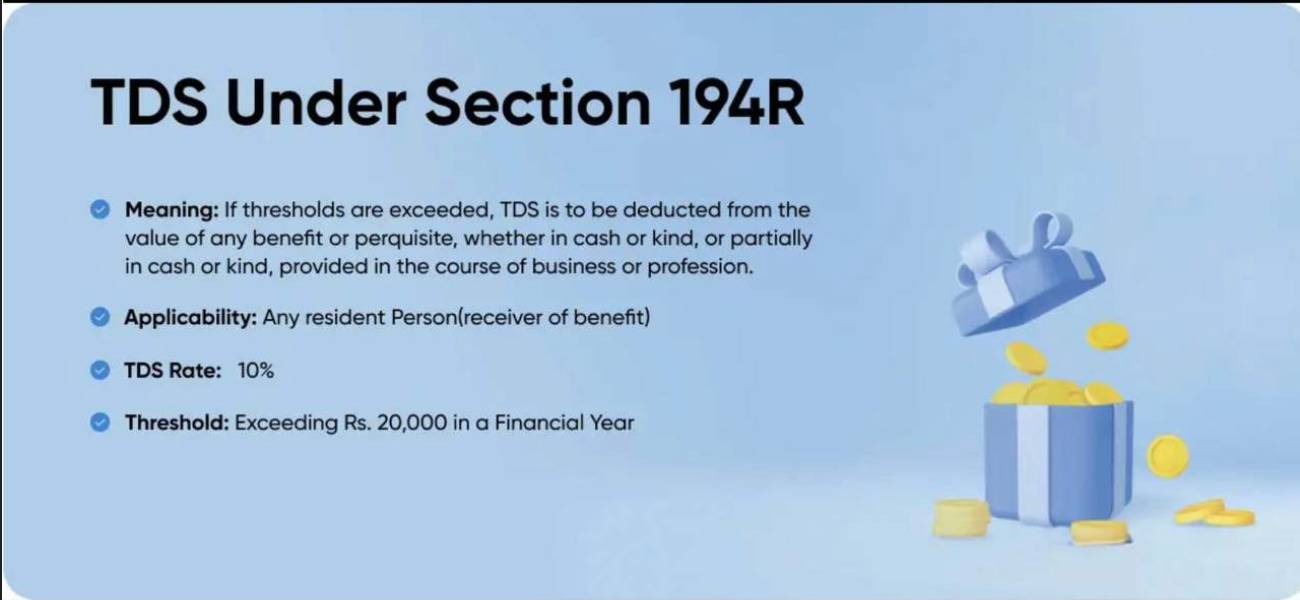

194R TDS: Rules, Rates, and examples explained Businesses that provide benefits or perquisites to residents must comply with Section 194R of the Income Tax Act's new compliance requirements. This requirement was introduced by the Government's Budget 2022 and ensures that tax must be deducted at source (TDS) from the provision of benefits or perquisites to increase transparency in Business Transactions with Residents. What is section 194R As mandated by Section 194R, any person who provides benefits or perquisites to residents as a result of their business or performance as a profession will be required to deduct TDS prior to providing the benefit. The intention of this section is to ensure the taxation of rewards for Non-Monetary Incentives, which were previously not taxed.

Therefore, with respect to any reward for dealers, distributors, or professional individuals such as gifts, incentives or any sponsored benefit, an entity must ensure that the Value of that benefit is subject to TDS deduction. The purpose of the introduction of this section was to increase the amount of transparency and accountability associated with business transactions and to ensure that all types of income (whether by way of cash or kind) are appropriately reported and taxed under the Income Tax Act.

Refer this: Section 194J - TDS on Professional Fees

Key features of section 194R TDS is applicable on any benefits or perquisites arising from the nature of business or profession, including bonuses, rewards, benefits, with respect to business transactions or in relation to professional relationships.

This only relates to residents of India. If a person is a resident taxpayer then he is liable to pay taxes on any benefit received from the above.

At the time of providing any benefit, TDS will need to be deducted before the benefit is provided. TDS needs to be deducted when the benefit is completely provided in whole or in part, in order to ensure that TDS is paid in a timely manner.

Benefits will include both cash and non-cash examples, such as gifts, vouchers, travel and so forth.

Threshold limit - TDS is only applicable when the total aggregate value of benefits provided exceeds ₹20,000 during a financial year.

Specific types of businesses and/or professionals must comply - Any business person or company whose total turnover/receipts (gross receipts) exceeds ₹1 crore for business, or ₹50 lakh for profession, must pay TDS on benefits they are providing.

Proper valuation of benefits - The value of the benefit will be determined by the fair market value (FMV ) of the benefit, which will assist in calculating the correct TDS to pay.

Who is required to deduct TDS Businesses or professional practitioners must deduct TDS if:

Their turnover is more than ₹1 crore (for a business) or ₹50,00,000 (for a profession).

The small business will be exempted from deducting TDS under Section 194R if they do not exceed either of the above limits.

In summary, every entity that provides benefits/perquisites to a person must deduct TDS. This includes companies, firms (partnership and LLP ) and individual entities if they exceed the respective turnover limit. In order to qualify for a requirement to deduct TDS, the entity must base their respective limits on the previous financial year.

Important rules to remember TDS applies to all types of benefits, both monetary and non-monetary TDS applies to all benefits, including gifts, free samples, etc. that are not in cash. Thus, businesses need to be careful to track all of those benefits.

TDS must be paid by the provider if the benefit is provided in kind If the benefit is entirely in kind, then the cost of TDS must be incurred by the provider. In this case, the company can either recoup from the recipient the amount of TDS that it has incurred, or gross up the benefit so that the value of the benefit is such that the TDS can be paid correctly.

Use FMV to determine value of benefits TDS should be calculated based on the fair market value of the benefit. The value that is assigned to the benefit should represent the actual amount that the benefit would have sold for in the open market so that TDS is accurately calculated and that the recipient does not underreport the value of the benefit.

Examples of section 194R Example one - A dealer receives a gift from a company worth ₹30,000, so it incurs a threshold of TDS deduction which is 10% of ₹30,000 and therefore TDS to be withheld at ₹3,000. If the dealer receives a gift from the company without TDS deduction, the company will have to "gross up" the gift amount to cover the TDS.

Example two - A company provides a foreign holiday worth ₹1,00,000 (TDS will thus be ₹10,000) to the distributor. Since this is an entirely non-cash benefit, TDS will need to be withheld by the company before providing the benefit to the distributor. In such cases, the company typically withdraws TDS from their funds to ensure compliance with tax laws.

Example three - A distributor receives ₹18,000 in goods and later receives additional benefits in the form of goods or services valued at ₹5,000. Therefore, the entire amount, ₹23,000 (greater than the threshold of ₹20,000), will be subject to TDS. As a result, once the threshold is reached for a financial year, TDS will apply to the total amount for that financial year and not just to any amounts over the threshold.

When is TDS deducted TDS will be deducted:

Before the delivery of benefit/perquisite to the recipient

This ensures that the tax is collected as soon as possible, thus reducing potential revenue loss.

The provider is responsible for deducting or arranging for TDS to be deducted from any benefits provided to a recipient prior to actually providing the benefit (cash or otherwise) in question, regardless of whether the benefit is in cash or other form. If the benefit will be provided solely in non-cash form (gifts or travel) to a recipient, the provider should ensure TDS has been paid or will be collected from the recipient before providing the benefit in non-cash form.

Types of benefits covered under section 194R Type of Benefit Description Free products or samples Goods provided without charge for promotion or marketing purposes Gift vouchers Coupons, gift cards, or redeemable vouchers given as incentives Foreign trips sponsored by companies Travel, accommodation, or leisure trips funded by the business Incentives to dealers/distributors Rewards or perks given for achieving sales targets Bonus items in business transactions Additional goods provided along with regular purchases

Conclusion To ensure proper taxation of benefits and perquisites, section 194R is important as it requires businesses to properly monitor all transactions for compliance with TDS provisions to avoid penalties. To achieve such compliance smoothly and avoid any legal difficulties, businesses should be familiar with the rules, rates and examples associated with section 194R.

Suggested Read: Section 194H Of Income Tax - TDS on Commission and Brokerage

FAQs What does "section 194R" mean for TDS? A TDS that will be deducted from business or professional transactions for the benefit of either party.

What is the TDS rate under section 194R? The TDS rate on benefits provided is 10 percent of the benefit's value.

What is the threshold limit under section 194R? TDS is applicable to benefits provided only if the aggregate of those benefits provided during the tax year exceeds Rs 20,000.

Are non-cash benefits subject to tax under Section 194R? Yes, TDS is applicable to both cash and non-cash benefits.

Who is exempt from Section 194R? Applications that have an income turnover of less than Rs 1,00,00/Rs 50,000 for their business/profession, respectively, are exempt from this provision.

.png)

-compressed.jpg)

.jpg)